Navigating the Economic Tides: A Guide to Understanding Economic Cycles and Surviving Inflation

Have you ever walked out of a grocery store feeling bewildered? You bought the same items as last month, yet your bill is noticeably higher. Or perhaps you feel a knot of anxiety when news headlines scream about “recession fears” and “rising interest rates.”

If so, you are not alone. These are the tangible, everyday symptoms of massive macroeconomic concepts: The Economic Cycle and Inflation.

We live within an economic system that is constantly in motion, much like the respiratory system of a living organism. It inhales (expands) and exhales (contracts). Understanding this rhythm is not just for Wall Street experts; it is the key to alleviating anxiety and making smart financial decisions that protect your hard-earned labor.

This article will decode these concepts in simple terms and provide you with a “compass” to navigate through periods of economic turbulence.

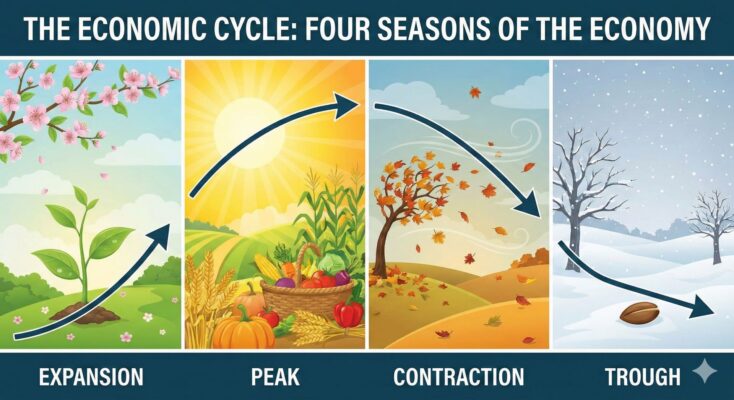

Part 1: The Economic Cycle – The Four Seasons of the Economy

The economy never stands still. It oscillates between periods of robust growth and periods of quiet struggle. This natural fluctuation is known as the economic cycle (or business cycle).

Think of the economic cycle as the four seasons of the year. No season lasts forever, and a harsh Winter is inevitably followed by a warm Spring.

A standard economic cycle typically moves through four main phases:

1. Expansion (Growth – Spring & Early Summer)

This is the “honeymoon phase” of the economy.

-

Characteristics: Businesses are thriving, and corporate profits are rising. Demand for labor is high, leading to low unemployment rates. Consumers feel optimistic, confident enough to spend money on homes, cars, and vacations. Banks are generally willing to lend capital.

-

Psychology: Euphoria, confidence in the future.

2. Peak (The Boom – Late Summer)

The economy is firing on all cylinders. This is when things look their best, but it is also when risks begin to accumulate.

-

Characteristics: Growth hits its maximum limit. However, because demand is so high while production capacity is limited, prices for goods and services begin to climb rapidly. This is the point where inflation often spikes (we will discuss this in detail later). Central banks start to worry and may begin raising interest rates to “tap the brakes.”

-

Psychology: Still optimistic, but caution begins to creep in among savvy investors.

(Image Suggestion 1: A sine wave chart depicting the 4 stages of the economic cycle, with clear labels for Expansion, Peak, Contraction/Recession, and Trough.)

3. Contraction (Recession – Autumn)

After peaking and feeling the impact of higher interest rates, the economy begins to cool down.

-

Characteristics: Consumers tighten their belts due to high prices and expensive borrowing costs. Businesses see revenue drop, leading to cost-cutting measures, halted expansion, and layoffs. Unemployment rates begin to rise.

-

Psychology: Anxiety, pessimism, shifting to “defense mode.”

4. Trough (The Bottom – Winter)

This is the lowest point of the cycle.

-

Characteristics: Economic activity is stagnant. Unemployment is high, and weaker businesses may go bankrupt. However, the silver lining is that inflation usually drops significantly during this phase. Central banks will eventually lower interest rates to “inject life” back into the economy, setting the stage for a new expansion.

-

Psychology: Despair, but this is also when the seeds of new opportunity are planted.

Crucial Note: The duration of these phases is not fixed. Some expansions last a decade, while some recessions are short but sharp.

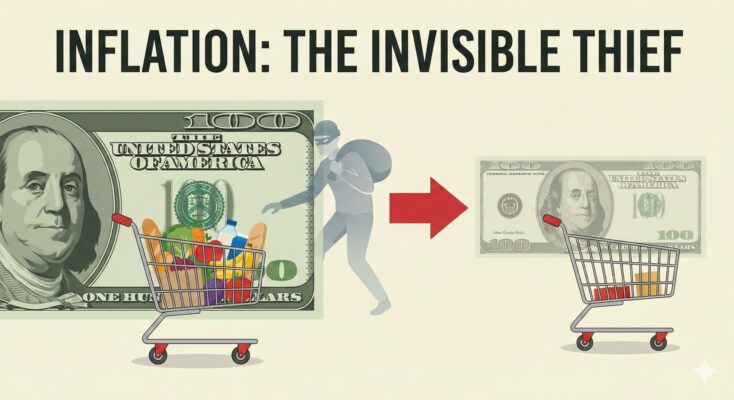

Part 2: Inflation – The Invisible Thief

In the grand picture of the economic cycle, inflation is a critical piece, usually most prominent during the Expansion and Peak phases.

What is Inflation?

In the simplest terms, inflation is the increase in the general price level of goods and services over time. This translates directly to a decrease in the purchasing power of your money. A $100 bill today buys fewer groceries than a $100 bill did ten years ago. That is inflation at work.

Inflation acts like an “invisible thief,” silently eroding the value of the assets you hold in cash.

Why Does It Happen?

While complex, the causes generally revolve around two main drivers:

- Demand-Pull Inflation (Too much money, too few goods):When the economy is expanding, people have more money and want to buy more things. If factories and service providers cannot produce enough to keep up with this surging demand, prices go up. Imagine ten people bidding on the last loaf of bread; the price will inevitably rise.

- Cost-Push Inflation (Production gets expensive):When the cost of doing business rises (e.g., oil prices spike, raw materials become scarce, or wages increase), companies are forced to raise the prices of their products to maintain margins. The consumer is the one who ultimately pays the bill.

(Image Suggestion 2: A visual comparison. On the left, a shopping cart overflowing with goods labeled “Past – $100”. On the right, a shopping cart half-empty labeled “Present – $100”, illustrating lost purchasing power.)

Is Inflation Good or Bad?

A mild, stable inflation rate (usually around 2-3% annually, depending on the country) is considered a sign of a healthy economy, as it encourages spending and investing rather than hoarding cash.

However, high or hyperinflation is a dangerous disease. It makes the population poorer, causes social instability, and paralyzes long-term business planning because no one can predict future costs. This is when you must take action to protect yourself.

Part 3: Taking Action – A Survival Strategy for Inflationary Times

Once you understand that high inflation usually accompanies the Peak of the cycle and is often followed by a Contraction, you must switch to “financial defense mode.”

Here are the principled actions you need to take to protect your wallet. Note: These are general guidelines, not specific financial advice.

1. Audit and Tighten the Budget (Core Defense)

During inflation, the price of everything from vegetables to electricity rises. If you maintain your old spending habits, you will quickly find yourself running a deficit.

-

The Action: Track every single expense for one month. Categorize them into “Needs” (housing, basic food, utilities, transport) and “Wants” (dining out, entertainment, impulse buys).

-

The Goal: Ruthlessly cut the “Wants.” Cook at home more often; find cheaper alternatives for subscriptions or services. Every dollar saved now is worth more than usual because it provides a buffer against rising costs.

2. Smart Debt Management (Avoid the Interest Trap)

To fight inflation, Central Banks use their most powerful tool: Raising Interest Rates. This means borrowing money becomes expensive.

-

The Action: If you have debts with variable interest rates (e.g., credit card debt, adjustable-rate mortgages), be extremely cautious. As rates rise, your monthly payments can skyrocket.

-

The Goal: Prioritize paying off high-interest debt immediately. Do not carry a balance on credit cards. Try to avoid taking on new debt during periods of rising rates unless absolutely necessary.

3. Protecting Purchasing Power (Safe Havens)

Leaving all your wealth in a checking account or under a mattress when inflation is at 8% means you are losing 8% of your wealth’s real value every year. You need to find a “shelter” for your capital.

-

Investment Principle during Inflation: Focus on assets with intrinsic value or businesses that have “pricing power” (the ability to raise prices without losing customers).

-

Potential Channels (Requires Research):

-

Consumer Staples: Invest in companies that produce things people must use regardless of the economy (electricity, water, basic food, healthcare, toiletries). These companies can usually pass higher costs onto consumers.

-

Real Assets (Real Estate, Gold): Historically, real estate and gold are viewed as hedges against inflation. However, real estate requires large capital and is hard to sell quickly (low liquidity). Gold should be viewed as insurance for a small part of your portfolio, not a get-rich-quick scheme.

-

Inflation-Protected Bonds: Some governments issue bonds where the principal value is adjusted based on the inflation rate (like TIPS in the US).

-

Crucial Warning: Stay away from “get rich quick” schemes or unregulated platforms promising “guaranteed high returns.” During economic volatility, scammers are most active, preying on people’s fear and desire to recover losses. Prioritize the safety of your principal over aggressive profits.

(Image Suggestion 3: A person sitting at a desk with a calculator, focused on a ledger or laptop, with a piggy bank and a “Financial Plan” notebook nearby.)

4. Upgrade Your Own Value (Investing in Human Capital)

This is the only investment that can never go to zero and is the best defense against long-term inflation.

-

The Action: Inflation raises the cost of living, so you need to raise your income. Learn a new high-demand skill, improve your professional qualifications to negotiate a raise, or start a side hustle (freelance work) to diversify your income streams.

-

The Goal: Become a high-value asset in the labor market. Ideally, you want your income growth to outpace, or at least match, the rate of inflation.

Final Thoughts

Economic cycles and inflation are inevitable laws of the financial universe. We cannot change the direction of the wind, but we can certainly adjust our sails.

Instead of panicking at inflation figures or recession forecasts, view them as the “Winter” of the economy. By equipping yourself with knowledge, maintaining budget discipline, managing debt wisely, and investing in real value, you will not only survive the storm of high prices but also position yourself to seize significant opportunities when the economic “Spring” returns.

Would you like me to help you create a simple monthly budget template to start tracking your expenses today?